Perhaps you have always been a careful budgeter, accounting for every dollar earned and penny spent. Or, maybe you have never focused closely on your household budget. Either way, the Coronavirus crisis and its economic impact on millions of Americans has highlighted the importance of budgeting and building an emergency fund.

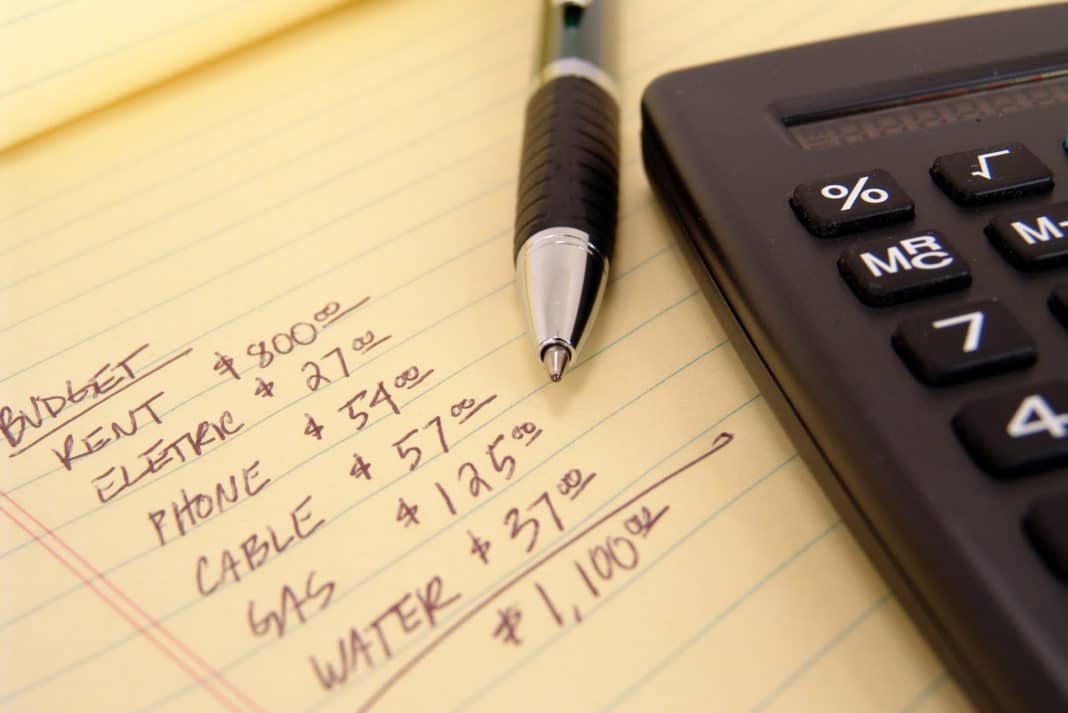

There are several different approaches to creating a household budget. For the do-it-yourselfer, a simple spreadsheet, a ledger book or the envelope system, where you place cash you earn in envelopes labeled with your spending categories, will suffice. For the tech-savvy, there are numerous websites and apps that can help you create and stick to a budget, track spending and savings, and monitor your financial goals.

The basic idea of a budget is to track your income and all expenses. On the income side, be sure to include salaries, interest and dividends, as well as income from any side jobs or other sources. For expenses, include fixed monthly bills as well as variable expenses. Be sure to include essentials (needs) as well as non-essentials (wants), and account for unexpected surprises and occasional costs such as gifts and travel.

Shutdown Highlights Need for Emergency Funds

The shutdown of the economy, an essential public health step to help flatten the curve and reduce the very real potential for the healthcare system to become overwhelmed with Covid-19 cases, unfortunately had a devastating effect on the financial well-being of millions of Americans. Many took advantage of assistance offered by the federal government: stimulus checks paid directly to individuals, additional dollars added onto weekly unemployment checks, and loan programs offered to small business owners. At the same time, many lenders including mortgage, credit card and insurance companies offered forbearance or deferred payment plans for their customers.

As the economy slowly begins to reopen, the time is right to assess your own family’s financial situation to determine how well you weathered the storm, and what changes you may want to make to ensure that you are well positioned to withstand any future emergencies.

Creating an Emergency Fund

Financial experts recommend keeping an emergency fund of three-to-six months’ worth of expenses on hand. This fund should be kept in a separate bank account and should be used only to help with unforeseen and unplanned expenses. Your emergency fund is separate and apart from other funds that you may be saving to use toward a vacation, major purchase, tuition or retirement.

While that amount may seem daunting, creating a budget can help you set aside a small amount of money each week or so as you work toward your goal. The money in your emergency fund should be kept in a savings account or money market account where it is easily accessible. Since this means that you will likely be earning a small rate of return on this money, experts caution that you avoid over-funding this account.

Start Small

It can take time to build three-to-six months’ worth of expenses in an emergency fund. Don’t let the goal overwhelm you. Start small, with $500 to $1000, and build from there. And keep in mind that the actual amount you save is totally up to you and dependent on your financial stability, employment situation and comfort level.

Feel free to reach out to us for assistance or questions about budgeting, saving and bill paying.